Foldable smartphones promise a future where one device replaces both your phone and tablet, and that vision is undeniably exciting for gadget enthusiasts.

However, many users hesitate right before hitting the buy button, wondering whether these futuristic devices can truly survive everyday use, travel, and changing environments.

If you are investing well over $1,500 in a cutting-edge foldable, durability is not a minor detail but a deciding factor that directly affects long-term satisfaction and resale value.

In recent years, manufacturers such as Samsung, Google, Honor, and Motorola have made significant engineering progress, yet concerns around fragile displays, complex hinges, dust resistance, and cold-weather failures continue to surface in real-world usage.

Beyond physical durability, there is also an economic dimension that many buyers overlook, including costly repairs, rapid depreciation, and limited resale demand.

This article carefully examines the structural, environmental, and financial durability of modern foldable smartphones in 2025–2026, using verified industry data, lab tests, and documented user experiences.

By the end of this guide, you will clearly understand where foldables truly stand today, what risks remain, and whether owning one makes sense for your lifestyle and usage patterns.

- Why Foldable Smartphones Are Facing a Durability Trust Gap

- Ultra-Thin Glass Explained: Strength Gains and Physical Limits

- Hinge Engineering Evolution and Real-World Stress Points

- IP Ratings Demystified: Why Dust Resistance Still Matters

- Cold Weather Risks and Material Behavior at Low Temperatures

- Durability Breakdown by Brand and Model

- Repair Costs, Insurance, and the Hidden Price of Ownership

- Depreciation and Resale Value Compared to Traditional Flagships

- What Tri-Fold Devices and Apple’s Entry Could Change

- 参考文献

Why Foldable Smartphones Are Facing a Durability Trust Gap

Foldable smartphones promise a dramatic leap in usability, yet many potential buyers hesitate at the final moment. The core reason is a durability trust gap that has widened rather than narrowed as the category has matured. According to Counterpoint Research, shipment forecasts for foldable displays were revised downward in 2025, and analysts consistently point to durability anxiety as the single strongest brake on mainstream adoption.

This gap is not rooted in vague fear but in a visible mismatch between price and perceived reliability. Devices that often exceed $1,500 are expected to survive years of daily stress, yet early and mid-generation foldables left a strong psychological imprint. Reports of screen protector peeling, crease discoloration, or hinge noise continue to circulate on social media, and these narratives linger far longer than official improvement claims.

In other words, consumer memory is cumulative, while trust is fragile. Even when manufacturers demonstrate better lab results, real-world anecdotes still shape perception more powerfully than specifications.

| Factor | What brands communicate | What consumers perceive |

|---|---|---|

| Hinge durability | 200,000–500,000 fold tests by certified labs | Unclear resistance to drops and dust |

| Display material | Ultra-Thin Glass replacing plastic | Still feels softer than slab smartphones |

| Ingress protection | IPX8 or IP48 water resistance | Dust and sand remain scary unknowns |

Authoritative institutions such as the IEC clearly define IP ratings, yet the nuance is rarely absorbed by consumers. For example, an IP48 rating technically allows particles smaller than 1.0 mm to enter the device. To engineers this is a known limitation, but to buyers it feels like a broken promise once they realize beach sand or pocket lint can still threaten a $2,000 phone.

Economic consequences amplify this distrust. SellCell’s resale studies show foldables losing close to 60 percent of their value within six months, nearly double the depreciation of flagship slab phones. This transforms durability from a physical concern into a financial one, reinforcing the fear that a single accident could erase most of the device’s worth.

Until foldables demonstrate not only improved engineering but also long-term value stability in everyday environments, this trust gap will persist. The technology may be advancing steadily, yet consumer confidence moves at a much slower, more emotional pace.

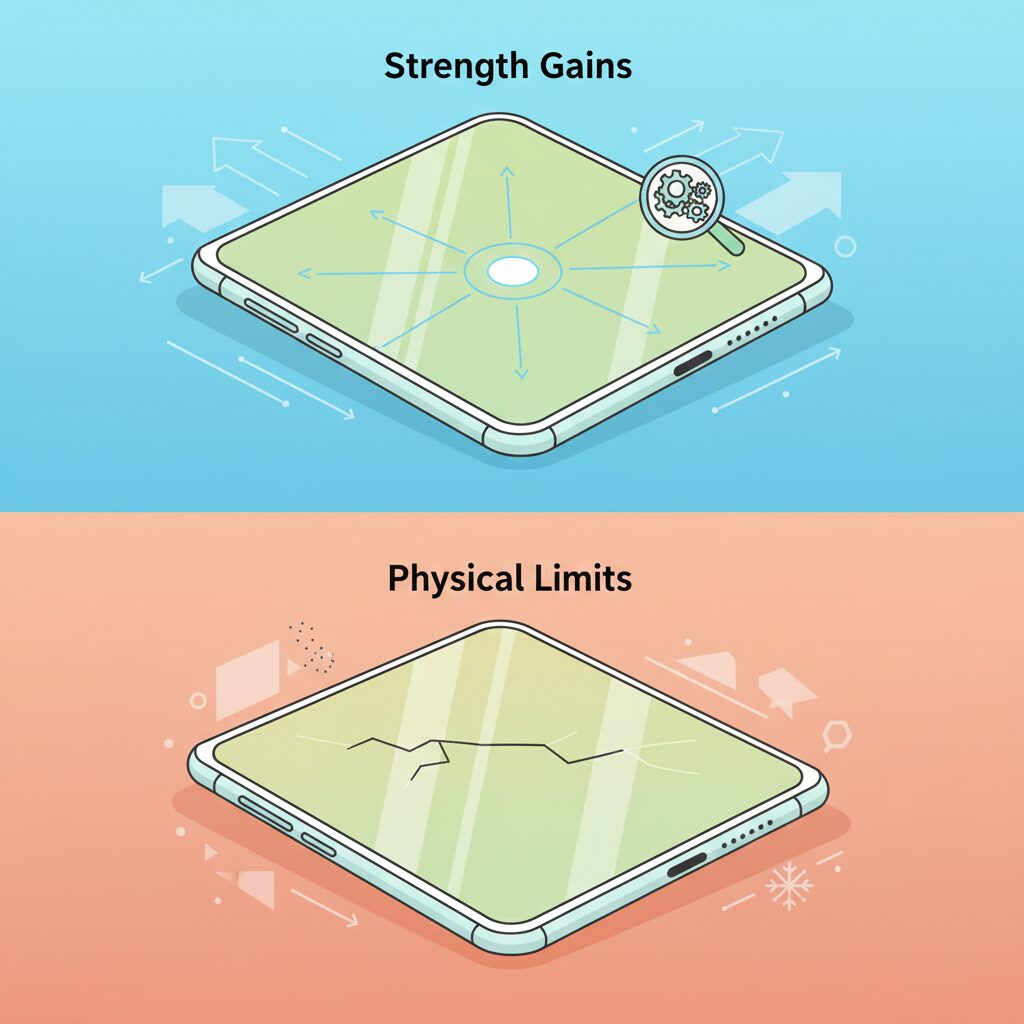

Ultra-Thin Glass Explained: Strength Gains and Physical Limits

Ultra-Thin Glass, commonly abbreviated as UTG, sits at the very core of modern foldable smartphones, and its evolution directly shapes both durability gains and unavoidable physical limits. Unlike early-generation plastic-based displays, today’s foldables rely on chemically strengthened glass supplied by specialists such as Schott and integrated by display leaders like Samsung Display. As of 2025, mainstream UTG thickness ranges from approximately 30 to 50 micrometers, thinner than a human hair, a fact frequently highlighted by materials scientists when explaining why glass can bend without immediately shattering.

The key strength improvement of UTG comes from controlled thinning rather than added hardness. By reducing thickness, glass transitions from a rigid, brittle plate into a flexible sheet capable of enduring repeated bending. According to supply-chain analyses published by Omdia and Patsnap, this shift has enabled foldable displays to survive hundreds of thousands of open-close cycles in laboratory testing. However, these gains are not linear, and they come with clear trade-offs that often remain invisible in marketing narratives.

| UTG Thickness | Flexibility | Puncture Resistance |

|---|---|---|

| 50 μm | Moderate | Relatively higher |

| 30 μm | High | Noticeably lower |

| 20 μm (target) | Very high | Significantly reduced |

As this comparison illustrates, thinner UTG improves crease visibility and bending endurance, but it also weakens resistance to localized pressure. Materials engineers describe this as a classic hardness–flexibility paradox. Schott’s publicly discussed roadmap points toward 20-micrometer UTG at mass-production scale, yet the company itself acknowledges that ultra-thin glass becomes increasingly vulnerable to point impacts, such as fingernails, debris, or stylus tips.

This vulnerability explains why UTG is never used alone. It is laminated with polymer protective layers and bonded to OLED panels using optical clear adhesives. Real-world durability issues often emerge not from the glass itself, but from degradation at these interfaces. Independent user studies and long-term field reports, including analyses of the Galaxy Z Fold series, repeatedly identify protective layer peeling along the crease as a precursor to deeper structural damage. Once separation begins, stress concentrates on the underlying UTG, increasing the probability of micro-cracks.

Display researchers also note that design decisions intended to improve efficiency can indirectly raise risk. For example, the removal of polarizer layers in Eco2 OLED structures reduces thickness and power consumption, but it also means external forces propagate more directly to the glass substrate. Similarly, stylus compatibility requires additional digitizer layers, adding complexity and new stress boundaries. Samsung’s insistence on using only specially designed S Pens with retractable tips is a tacit acknowledgment of UTG’s sensitivity to concentrated force.

In short, UTG has made foldable smartphones viable, but not invincible. Its strength gains are real and measurable, yet they operate within strict physical limits defined by materials science. As leading academic and industrial research consistently shows, no amount of chemical strengthening can fully offset the risks introduced by extreme thinness. Understanding this balance is essential for readers who want to separate genuine technological progress from unrealistic expectations surrounding foldable display durability.

Hinge Engineering Evolution and Real-World Stress Points

The hinge is the mechanical heart of a foldable smartphone, and its evolution over the past few generations has been driven less by elegance and more by survival under real-world stress. Early designs relied heavily on complex gear assemblies, which distributed load predictably but created multiple friction points. Modern designs have shifted toward gearless or semi-floating structures that rely on controlled friction and multi-link plates to guide the folding radius more gently.

This transition has reduced visible creasing and improved smoothness, but it has also introduced new stress concentrations. According to durability certifications conducted by organizations such as SGS and Bureau Veritas, hinges can now withstand 200,000 to 500,000 folding cycles under laboratory conditions. However, these tests assume clean environments and uniform motion, which rarely reflect daily use.

| Design Focus | Engineering Benefit | Real-World Weakness |

|---|---|---|

| Gear-based hinges | Stable angle control | Dust accumulation and wear |

| Gearless hinges | Thinner profile | Higher sensitivity to impact |

| Sweeper mechanisms | Debris mitigation | Ineffective against micro-dust |

Field reports and teardown analyses from professional reviewers indicate that lateral shocks, such as drops onto the hinge edge, remain the most catastrophic failure mode. Even reinforced materials like Armor Aluminum or proprietary high-strength steels cannot fully absorb torsional forces once the hinge axis is misaligned.

What is often overlooked is cumulative micro-stress. Slight resistance during opening, barely perceptible wobble, or subtle acoustic changes can signal internal wear long before failure becomes visible. Mechanical engineers interviewed by display industry analysts have noted that hinge fatigue is rarely sudden; it is progressive and accelerated by environmental contamination.

As foldables chase thinner profiles and more ambitious form factors, hinge engineering is increasingly a balancing act rather than a solved problem. The technology has matured, but the margin for error in everyday handling remains far narrower than with conventional smartphones.

IP Ratings Demystified: Why Dust Resistance Still Matters

When manufacturers advertise IP ratings on foldable smartphones, many readers understandably focus on water resistance. However, in daily use, dust resistance often matters more, and it is also far easier to misunderstand. Especially for foldables with complex hinge mechanisms, the difference between perceived protection and actual protection can quietly determine long-term reliability.

The IP code is defined by the International Electrotechnical Commission, a highly authoritative standards body. The first digit indicates protection against solid particles, while the second digit refers to water. **The critical point is that these numbers are not relative or marketing-driven; each digit corresponds to a very specific physical test condition.** This precision is exactly why misinterpretation becomes dangerous.

| Dust Rating | IEC Definition | What Still Gets Inside |

|---|---|---|

| IP4X | Blocks solids ≥ 1.0 mm | Fine sand, textile lint, household dust |

| IP5X | Limited dust ingress allowed | Dust over time under pressure |

| IP6X | Dust-tight enclosure | Practically none |

Recent foldables claiming IP48 certification represent an important step forward, yet the number “4” deserves careful attention. According to IEC documentation and widely cited engineering references, IP4X only prevents objects larger than 1.0 mm from entering. **Typical beach sand measures around 0.1–0.25 mm, and fabric lint can be even smaller.** In other words, the most common contaminants in pockets and bags are not covered at all.

This gap between expectation and reality explains why dust remains a leading cause of hinge degradation. Engineers interviewed by display supply-chain analysts consistently point out that micron-scale particles act like abrasives. Once trapped inside a hinge, they do not simply sit still; repeated opening and closing grinds them against metal and polymer surfaces, accelerating wear far beyond what lab-based cycle tests predict.

Independent teardown specialists, frequently cited by publications such as iFixit and CNET, have shown that even advanced “sweeper” or brush systems cannot fully eject fine particles. These systems are effective against visible debris but largely ineffective against powder-like dust. Over months of use, that residue migrates inward, sometimes reaching the underside of the ultra-thin glass and creating localized pressure points.

From a user perspective, dust resistance therefore has an outsized impact on resale value and perceived aging. Devices may remain functional, yet subtle symptoms appear: faint crunching sounds in the hinge, uneven opening angles, or micro-bulges along the crease. **None of these necessarily qualify as defects under warranty, but all of them reduce confidence and market value.**

For this reason, dust resistance should be read not as a safety guarantee but as a risk indicator. Until foldables achieve true IP6X-level sealing, careful handling around sand, fabric fibers, and dusty environments remains essential. Understanding what the IP rating actually promises allows owners to align expectations with physics, rather than with marketing reassurance.

Cold Weather Risks and Material Behavior at Low Temperatures

Cold weather introduces a distinct and often underestimated risk profile for foldable smartphones, because low temperatures directly change how key materials behave.

At the core of the problem is the fact that **glass, polymers, and adhesives all become stiffer and more brittle as temperatures drop**, while each material responds at a different rate.

This mismatch amplifies mechanical stress precisely at the fold line, where tolerances are already measured in micrometers.

According to materials science research cited by display suppliers such as Schott and Samsung Display, ultra-thin glass maintains flexibility at room temperature but rapidly loses strain tolerance below freezing.

The adhesives bonding UTG, protective films, and OLED layers are even more temperature-sensitive.

When these optical clear adhesives harden, they can no longer absorb shear stress during folding, causing force to concentrate at a single point.

| Component | Behavior Near 20°C | Behavior Below 0°C |

|---|---|---|

| Ultra-Thin Glass | Elastic within design limits | Higher fracture risk |

| Polymer Film | Flexible, impact-absorbing | Stiff, prone to cracking |

| Adhesive Layers | Stress-dispersing | Hardened, stress-concentrating |

User reports from cold regions consistently describe failures occurring not during drops, but during normal unfolding outdoors.

Manufacturers indirectly acknowledge this risk by specifying operating temperature ranges of roughly 0°C to 35°C in official safety guides.

Opening a foldable below that range is technically outside design assumptions, even if the device still powers on.

Rapid temperature changes worsen the situation.

Moving from sub-zero air into a warm indoor space can cause micro-condensation inside hinge cavities and along display layers.

Over time, this moisture accelerates adhesive degradation and corrosion, compounding the original cold-stress damage.

From a materials perspective, cold weather does not merely reduce durability.

It fundamentally shifts the mechanical balance that makes folding possible in the first place.

This is why winter usage remains one of the most critical, and least solvable, durability challenges for foldable smartphones today.

Durability Breakdown by Brand and Model

When durability is discussed at the brand and model level, important differences emerge that are not always visible in spec sheets or marketing claims. Real-world reliability is shaped by hinge philosophy, display stack design, environmental sealing, and the maturity of each manufacturer’s foldable program.

Among current players, Samsung stands out for accumulated empirical data. Independent testing bodies such as Bureau Veritas have certified more than 200,000 opening and closing cycles for recent Galaxy Z Fold and Flip generations, translating to roughly five years of heavy daily use. This does not make failures impossible, but it reduces uncertainty. **Samsung’s advantage lies less in absolute strength and more in predictable aging behavior**, something repair centers and insurers can already model.

| Brand / Model | Hinge Durability Claim | Dust / Water Rating | Observed Weak Points |

|---|---|---|---|

| Samsung Galaxy Z Fold 6 | 200,000+ cycles certified | IP48 | Inner film peeling, hinge impact sensitivity |

| Google Pixel 9 Pro Fold | Not publicly certified | IPX8 | Display signal instability, hinge rigidity |

| Honor Magic V3 | 500,000 cycles (SGS) | IPX8 | Thermal buildup, service availability |

| Motorola Razr 50 Ultra | Undisclosed | IPX8 | Film wear history, hinge play over time |

Google’s Pixel 9 Pro Fold represents a different durability profile. The move to a fully flat-opening hinge improved usability, but early user reports collected through Google support forums suggest intermittent display failures and touch issues. These are not catastrophic in volume, yet they indicate **integration risk between hardware tolerances and software calibration**, a challenge Google is still resolving in its second-generation hardware.

Honor’s Magic V3 takes a more aggressive engineering route. With a titanium-reinforced hinge and SGS-rated 500,000-fold certification, it appears mechanically robust on paper. However, industry analysts and teardown specialists note that extreme thinness constrains heat dissipation. Over prolonged thermal stress, this can accelerate adhesive fatigue within the display stack. **Durability here is conditional: excellent under ideal use, less forgiving under sustained load.**

Motorola’s Razr 50 Ultra highlights how form factor influences longevity. As a clamshell device, it naturally reduces exposure of the main display when carried. Reviewers from established photography and hardware publications have noted that its large outer screen lowers fold frequency, which can extend hinge life. At the same time, Motorola’s historical issues with protective film cracking still shape consumer perception, making long-term confidence slower to recover.

Authoritative market researchers such as Counterpoint Research emphasize that consumer hesitation in 2025–2026 is driven by variance, not averages. Some units perform flawlessly for years, while others fail early without obvious misuse. **This spread in outcomes differs by brand maturity**, with Samsung showing the narrowest range and newer entrants exhibiting wider dispersion.

Ultimately, a durability breakdown by brand reveals that foldables are converging mechanically but diverging operationally. Buyers are not choosing between “durable” and “fragile” devices anymore. They are choosing between predictable durability, experimental durability, and conditional durability, depending on how each manufacturer balances thickness, heat, sealing, and long-term support.

Repair Costs, Insurance, and the Hidden Price of Ownership

When discussing foldable smartphones, repair costs and insurance are not side notes but central pillars of ownership experience. The complex integration of ultra-thin glass, flexible OLED panels, and hinge assemblies means that a single point of failure often requires replacing an entire module rather than an isolated part. According to warranty and repair analyses summarized by SureBright and major manufacturers, a broken main display on a book-style foldable routinely results in repair quotes that rival the price of a midrange phone.

For many users, the fear is not that the device might break, but that the financial impact of a single accident is disproportionately large. Unlike slab-style smartphones, where front glass replacement is relatively standardized, foldable displays are custom-fitted components produced in lower volumes. This scarcity, combined with delicate installation procedures, directly drives up labor and parts costs.

Industry repair data from 2025 indicates that out-of-warranty inner screen replacements for popular foldables frequently fall in the range of several hundred US dollars, and in some cases approach half of the original retail price. Consumer protection groups and teardown specialists such as iFixit have repeatedly pointed out that the hinge-display interdependence leaves little room for partial repairs, reinforcing the “all-or-nothing” nature of service outcomes.

This economic reality explains why insurance uptake is dramatically higher among foldable owners than among conventional flagship users. In Japan, carrier-backed programs from NTT Docomo, SoftBank, and au are often cited by analysts as a hidden prerequisite for adoption. These plans cap repair fees at relatively modest amounts, transforming an unpredictable, high-impact risk into a predictable monthly cost. From a behavioral economics perspective, this risk smoothing plays a crucial role in purchase decisions.

| Scenario | Without Insurance | With Carrier Protection |

|---|---|---|

| Main foldable display damage | High three-digit repair bill or full replacement | Low, capped service fee |

| Hinge malfunction | Often treated as major repair | Covered under standard claims |

However, insurance does not eliminate all hidden costs. Claims often involve device swaps rather than same-unit repairs, which can lead to data migration downtime and temporary loss of customization. Experts in mobile lifecycle management also note that repeated claims may affect eligibility or increase long-term costs, an aspect rarely highlighted in marketing materials.

Beyond repairs, depreciation represents another less visible but equally important expense. Secondary market studies referenced by SellCell show that foldable phones lose value significantly faster than traditional flagships. Buyers discount heavily for potential hinge fatigue and unseen display wear, even when cosmetic condition appears excellent. As a result, resale value after one year can be dramatically lower than that of an equivalent non-foldable device.

This rapid depreciation effectively shifts the cost structure of ownership from long-term asset to short-term consumable. For enthusiasts who upgrade frequently, the loss may be acceptable. For mainstream users accustomed to trading in devices to subsidize upgrades, the numbers can be sobering.

Ultimately, the hidden price of foldable ownership lies in the intersection of high repair costs, mandatory insurance, and accelerated value loss. Analysts from Counterpoint Research have suggested that until repair modularity improves or durability perceptions stabilize, these economic factors will continue to suppress mass-market adoption. Foldables may represent the future of form factors, but today, they demand a more calculated financial mindset than almost any other smartphone category.

Depreciation and Resale Value Compared to Traditional Flagships

When discussing depreciation and resale value, foldable smartphones reveal a structural disadvantage compared with traditional flagship models. **High initial pricing combined with lingering durability concerns accelerates value erosion**, turning what looks like a premium asset into a rapidly depreciating one. Market analysts at SellCell and Counterpoint Research consistently point out that resale markets price not just specifications, but perceived long-term risk.

In practical terms, buyers discount foldables for uncertainty. Even when a device appears cosmetically perfect, hidden wear in the hinge mechanism or cumulative fatigue in the ultra-thin glass cannot be verified visually. This asymmetry of information mirrors what economists describe as a “lemon market,” where buyers assume worst-case scenarios and lower their offers accordingly.

| Device Category | Value After 6 Months | Primary Depreciation Driver |

|---|---|---|

| Foldable Flagship | ≈40% of launch price | Durability risk, repair cost |

| Traditional Flagship | ≈60–70% of launch price | Normal generational churn |

According to SellCell’s comparative resale studies, foldables lose roughly 60% of their value within six months, while devices like iPhone Pro or Galaxy S Ultra models typically shed only 30–40% in the same period. **This gap is not explained by performance or features**, but by buyer anxiety around hinges, internal displays, and future repair exposure.

Another compounding factor is repair economics. Authoritative teardown analyses and manufacturer service pricing show that replacing a foldable’s main display can cost close to half the original retail price. From a second-hand buyer’s perspective, this creates a ceiling on what the device is worth, regardless of how advanced it once was.

Traditional flagships benefit from predictability. Their slab design, standardized components, and long track record allow resale platforms and carriers to forecast failure rates with confidence. **Foldables, by contrast, are penalized for novelty**, even as engineering improves. Until durability perception catches up with innovation, depreciation will remain structurally steeper.

For consumers, this means ownership should be evaluated more like a consumable luxury than an appreciating asset. The value proposition lies in daily experience, not exit value. In resale terms, foldables ask users to accept faster write-offs in exchange for early access to a new form factor, a trade-off traditional flagships simply do not demand.

What Tri-Fold Devices and Apple’s Entry Could Change

Tri-fold devices represent a qualitative shift rather than a simple extension of existing foldables, and that distinction is important when considering what they could change for the market.

By introducing a second hinge, manufacturers such as Huawei and Samsung are effectively attempting to merge smartphones and tablets into a single, pocketable product.

This promise of a 10-inch-class display that unfolds from a phone-sized body directly challenges the long-standing boundary between mobile and PC-like productivity.

| Form Factor | Number of Hinges | Key Trade-off |

|---|---|---|

| Bi-fold (current mainstream) | 1 | Balanced usability and risk |

| Tri-fold | 2 | Larger screen vs. higher failure probability |

From a structural engineering perspective, however, the implications are sobering.

As multiple analysts have pointed out, each additional hinge is not just an extra moving part but an additional stress concentration point.

If a conventional foldable already struggles with dust ingress, adhesive fatigue, and cold-weather brittleness, a tri-fold design compounds all of these risks.

Early reports cited by SamMobile regarding display damage on prototype tri-fold devices, even without obvious external impact, reinforce the idea that this category is still in an experimental phase.

For consumers, this means tri-folds are unlikely to function as mass-market replacements for today’s phones in the near term.

Instead, they are better understood as technology demonstrators or status devices aimed at users who consciously accept higher risk in exchange for novelty and screen real estate.

Against this backdrop, Apple’s potential entry into the foldable market carries disproportionate symbolic weight.

Apple’s historical behavior, as noted by supply-chain analysts and repeatedly observed in past product categories, suggests that the company avoids being first and instead waits for key technologies to reach a reliability threshold.

If Apple launches a foldable device, it will implicitly signal that durability, crease management, and long-term usability have reached a level Apple considers acceptable for its mainstream audience.

This signal matters because Apple’s standards tend to reshape supplier roadmaps.

Ultra-thin glass manufacturers, hinge component suppliers, and adhesive specialists would all be forced to meet stricter tolerances, potentially accelerating improvements across the entire ecosystem.

According to industry observers referenced by Counterpoint Research, even rumors of Apple’s foldable plans have already influenced long-term investment decisions in display and materials research.

At the same time, Apple’s entry could recalibrate consumer expectations.

For many users, especially in markets with strong iPhone loyalty, the absence of Apple has reinforced the perception that foldables are inherently fragile or experimental.

An Apple-branded foldable would not eliminate physical limitations, but it could normalize the idea that folding devices are dependable enough for everyday use.

In this sense, tri-fold devices and Apple’s eventual participation point in opposite but complementary directions.

Tri-folds push the technical frontier outward, testing what is mechanically possible, while Apple is likely to consolidate inward, defining what is commercially and psychologically acceptable.

The interaction between these two forces will largely determine whether foldables remain a niche curiosity or evolve into a stable, trusted category over the next product cycle.

参考文献

- Counterpoint Research:Foldable Smartphone Market Stalls in 2024 and 2025

- SellCell:Foldables Fall Flat on Value Retention, New SellCell Data Shows

- Android Headlines:Samsung Foldable Displays Hit 500,000 Folds Durability Mark

- Honor:HONOR Unfolds a Future with Possibilities with the HONOR Magic V3 at IFA 2024

- Google Support:Safety & Regulatory Guide for Pixel 9 Pro Fold

- Electricsolenoidvalves.com:IP Ratings Explained: What They Mean and Why They Matter